Fixed vs. Adjustable-Rate Mortgages: Which Is Right for You?

6/5/20252 min read

Fixed vs. Adjustable-Rate Mortgages: Which Is Right for You?

When choosing a mortgage, one of the most important decisions you'll face is whether to go with a fixed-rate or an adjustable-rate mortgage (ARM). A fixed-rate mortgage offers stability, with an interest rate that remains the same for the life of the loan—typically 15, 20, or 30 years. This predictability makes it easier to budget, especially for first-time homebuyers or those planning to stay in their home long-term. Even if interest rates rise in the future, your monthly payment won’t change, which can offer peace of mind in an uncertain economy.

On the other hand, adjustable-rate mortgages usually start with a lower interest rate than fixed-rate loans, making them attractive to buyers looking to save money in the short term. However, after an initial fixed period—often 5, 7, or 10 years—the rate adjusts periodically based on market conditions. This means your monthly payments could increase or decrease over time. ARMs can be a smart choice for buyers who plan to move or refinance before the adjustment period begins, or for those who anticipate a rise in income that can accommodate potential payment increases.

Ultimately, the right mortgage depends on your financial goals, risk tolerance, and how long you plan to stay in the home. If you value consistency and plan to settle in for the long haul, a fixed-rate mortgage may be your best bet. But if you're comfortable with some uncertainty and want to take advantage of lower initial payments, an ARM could offer significant savings. Consulting with a mortgage advisor can help you weigh the pros and cons based on your unique situation and ensure you make the most informed decision.

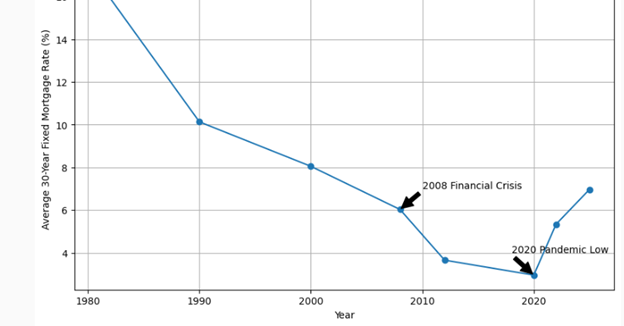

Chart showing average U.S. 30-year fixed mortgage rates for key years from 1981 to 2025, with major economic events annotated:

This visual highlights:

📈 The 1980s inflation peak at over 16%

📉 The 2008 financial crisis dip

🧊 The 2020 pandemic low under 3%

🔼 The 2025 rate climbing back to nearly 7%